- Home »

- Knowledge »

- Digital Assets »

- Investing in Cryptocurrencies

to read

Cryptocurrency Investments

Since the launch of Bitcoin in 2009, cryptocurrencies have evolved considerably during multiple market cycles. The dynamic ecosystem is experiencing phases of strong growth but also of restriction in cold “crypto winters”. While cryptocurrencies were originally mostly adopted by retail investors, institutional adoption has commenced over the last years. Large financial institutions are building cryptocurrency products and solutions, providing more and more investors access to the young ecosystem.

While there are thousands of cryptocurrencies, the market is still concentrated on the two largest ones, bitcoin and Ether, which over the last years have attracted around two thirds of the whole market capitalization. Bitcoin, the oldest and by far largest cryptocurrency, aims to offer innovative store of value and payment solutions. Ether, the second largest cryptocurrency, offers investors to profit from innovative new use cases built on the general purpose Ethereum infrastructure. “Altcoins”, referring to all other cryptocurrencies besides bitcoin and Ether, drive much innovation in the cryptocurrency ecosystem. While some of them could and likely will become much more relevant in the future, determining which ones could establish themselves as dominant cryptocurrencies is difficult

Cryptocurrency Dominance

Graphic: DWS International GmbH, 2024; Data source: Coinmarketcap, as of March 2024

Empirical assessment of bitcoin and Ether

The below section provides an overview of cryptocurrencies’ development by comparing the historical return, risk and correlation of cryptocurrencies and traditional asset classes. While cryptocurrencies have been around since 2009, the below analysis concentrates on the timespan between August 2017 and December 2023. On the one hand, this period cuts off data from the early beginnings, which are less representative for potential future developments. On the other hand, the chosen timespan starts with the period between 2017-2018, in which a big crypto bull and subsequent bear market led to mass crypto awareness and increasing institutionalization. Of course, as always and also in particular for the young cryptocurrency asset class, past performance is no indication for future developments.

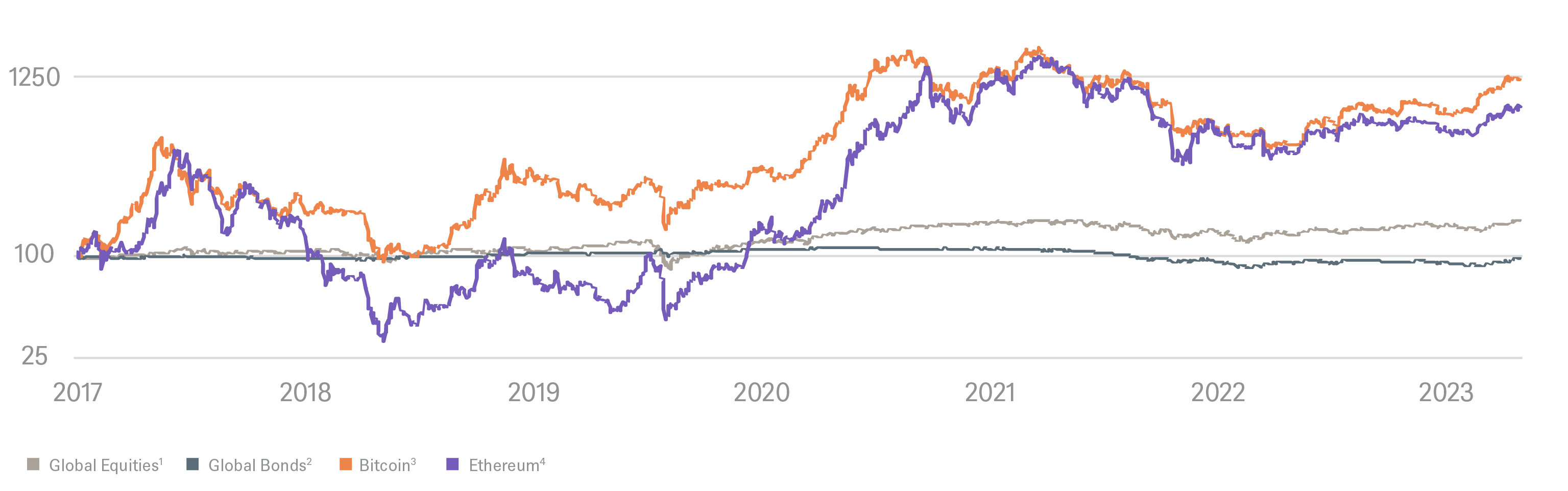

Daily returns (08/2017 – 12/2023, scaled to 100, semi-log scale)

Source: DWS International GmbH as of 02/2024; ¹MSCI AC World Index in USD; ²Bloomberg Global-Aggregate Total Return Index in USD; ³Bloomberg Galaxy Bitcoin Index in USD, ⁴Bloomberg Galaxy Ethereum Index in USD; past performance is not a reliable indicator of future results.

Very high absolute historical performance of bitcoin and Ether: Within the observation period, the price of bitcoin has multiplied by more than 12 and of Ether by more than 8 times, exceeding by far the performance of global equities and global bonds.

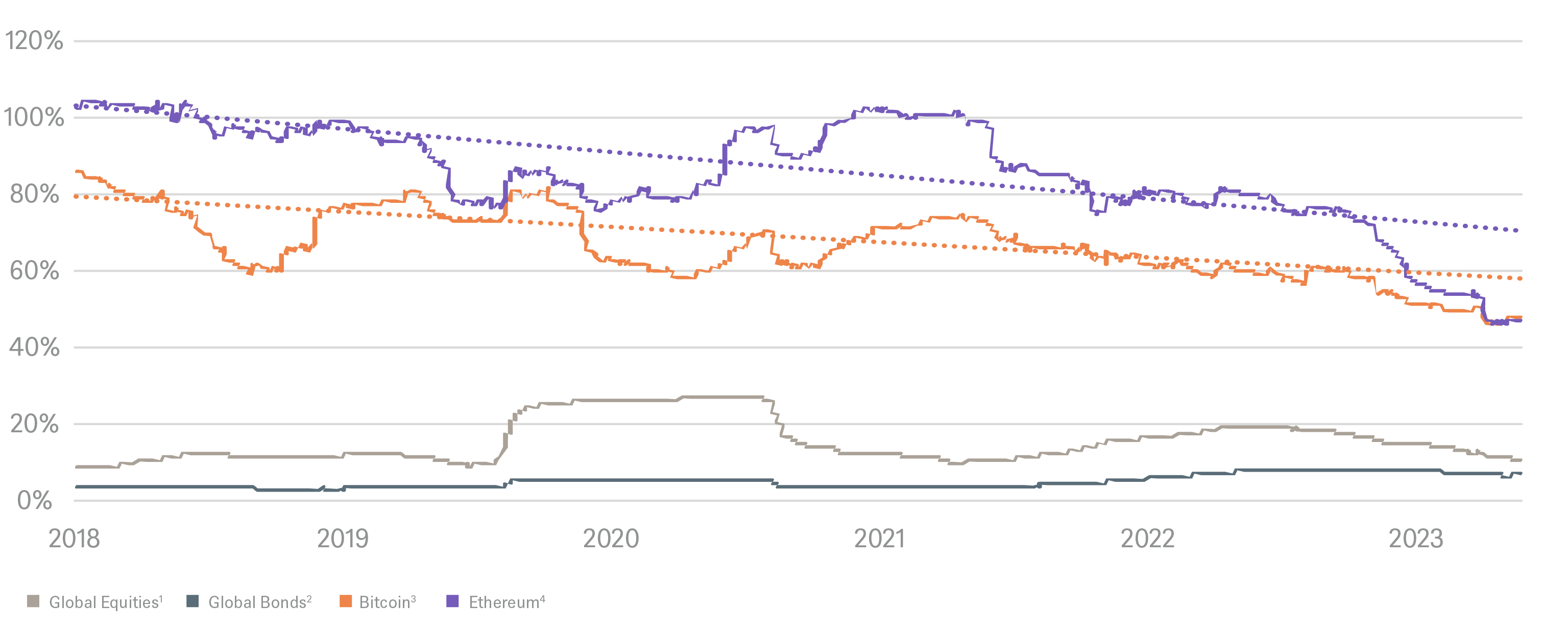

Rolling 1-year volatility (08/2017 – 12/2023)

Source: DWS International GmbH as of 02/2024; ¹MSCI AC World Index in USD; ²Bloomberg Global-Aggregate Total Return Index in USD; ³Bloomberg Galaxy Bitcoin Index in USD, ⁴Bloomberg Galaxy Ethereum Index in USD; past performance is not a reliable indicator of future results.

Bitcoin and Ether are highly volatil, as many other young assets. Bitcoin and Ether’s rolling 1-year volatility shows a high historical risk, with their volatility being 4-5 times higher as compared to global equities. Though bitcoin and Ether’s volatility has decreased in recent years, it remains high.

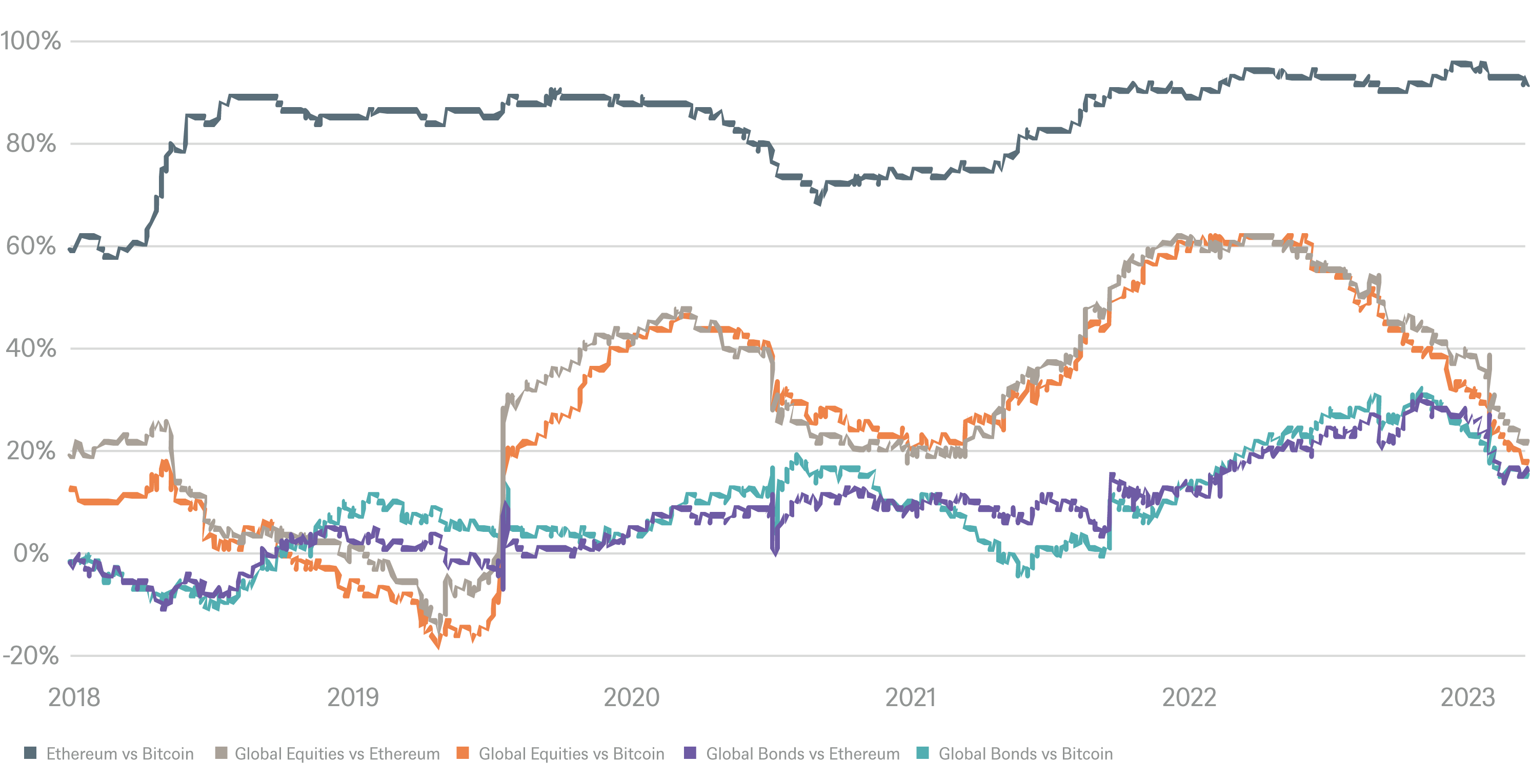

Rolling 1-year correlation of daily returns (08/2017 – 12/2023)

Source: DWS International GmbH as of 02/2024; Global Equities: MSCI AC World Index in USD; Global Bonds: Bloomberg Global-Aggregate Total Return Index in USD; Bitcoin: Bloomberg Galaxy Bitcoin Index in USD, Ethereum: Bloomberg Galaxy Ethereum Index in USD; past performance is not a reliable indicator of future results.

Bitcoin and Ether’s correlation with traditional asset classes is fluctuating but remains relatively low, which renders the two assets interesting for portfolio diversification. Bitcoin and Ether consistently strongly correlate with each other during the observation period.

Allocation considerations

The above historical data suggest that a small cryptocurrency allocation may be interesting for well-diversified investors. The increasing institutionalization, regulatory developments, and shifting macroeconomic circumstances further strengthen the case for a cryptocurrency allocation. Low correlations to traditional assets may offer diversification benefits despite higher volatility. A small cryptocurrency allocation within diversified portfolios may enhance overall returns. Nevertheless, given the industry’s early stage and rapid evolution, cryptocurrencies remain a risky growth asset. Investors should familiarize themselves with the risks to be able to make an informed investment decision.

Key risks include:

- Market and liquidity risks, especially the high volatility which is also increased by speculation

- Technical and operational risks, especially cryptocurrency custody and blockchain specific risks such as hacking attempts and sustainability risks. In addition, the ecosystem nascency and limited regulation lead to heightened counterparty risks including illicit activity risks.

- Regulatory risks due to emerging and changing national and regional regulatory requirements within the global cryptocurrency ecosystem

Did you know facts

- Cryptocurrencies are one of the few, if not the only, major financial innovations that were first adopted by retail investors. Nonetheless, institutional adoption has increased over the last years.

- Like any other asset, cryptocurrency prices are determined by supply and demand. Bitcoin’s supply schedule is fixed and has an absolute cap of 21 million bitcoin. Ethereum’s supply schedule is known but not fixed, the Ether supply can be inflationary and deflationary.

- It is estimated that about 10-20% of all bitcoins that will ever be in circulation are probably lost forever due to the loss of the corresponding private keys, which underlines the importance of private key custody[1].

- About 4% of the population are estimated to own cryptocurrencies[2].

- Each year, the Bitcoin community celebrates the “Bitcoin Pizza day”, which marks the anniversary of the first commercial bitcoin transaction ever: On May 22 2010, two pizzas were bought for 10,000 bitcoin, which then equaled 30 USD, but today would equal hundreds of millions. Let’s hope the pizzas were tasty!

Past performance is not a reliable indicator of future results.

The Importance of cryptocurrency custody

Cryptocurrencies are stored on their corresponding blockchains: A bitcoin is stored on the Bitcoin blockchain, an Ether is stored on the Ethereum blockchain. Cryptocurrencies are managed through “wallets” which do not store the cryptocurrency itself, but instead provide access rights to the cryptocurrencies. Access rights are managed through a matching pair of public and private keys, which are both long alphanumeric codes. While the public key functions like a bank account number and can be freely shared, the corresponding private key works like a bank account pin: It serves as a digital signature to authorize cryptocurrency transfers. If private keys are lost - and if no backup is available - access to the cryptocurrencies is irretrievably lost forever. It is therefore of vital importance to ensure that private keys are kept safe and never lost. Cryptocurrency custody enacts the safekeeping for the private keys.

How can investors store their private keys?

Investors can choose whether to store their private keys themselves or delegate private key management to a custodian.

Self-custodial wallets |

Custodial wallets |

|---|---|

|

Investors manage their own private keys. The private key could simply be written on a piece of paper or be stored in more sophisticated soft- or hardware wallets. Hardware wallets can look similarly to USB sticks and can for example be kept in a physical safe. Investors must understand their responsibility for their private keys. Once lost, and without backup, the investment is lost irretrievably. |

Investors assign private key management to a trusted third party like a cryptocurrency exchange or a cryptocurrency custodian. Such parties should secure the private keys through highly sophisticated technical, operational and physical key management procedures and facilities. They often divide the private keys into multiple encrypted shards and have multiple private key backups in different high-security locations. |

Both self-custodial and custodial wallets can be "hot" and "cold". Hot wallets are connected to the internet, which enables faster authorization of cryptocurrency transfers but generally have a higher hacking risk. In contrast, cold wallets store the private keys offline and are therefore generally less likely to be hacked. However, the intentional friction delays authenticating cryptocurrency transfers.

Different ways to gain cryptocurrency exposure

Investors can choose between different options to gain cryptocurrency exposure. Two popular options are direct investments and investments via financial instruments, such as cryptocurrency ETCs. The table below provides a comparison:

Direct investment |

Investment via cryptocurrency ETCs |

|

|---|---|---|

Investment |

Investors directly buy cryptocurrencies |

Investors buy a cryptocurrency ETC that is backed by cryptocurrencies |

Access |

Self-custodial or custodial wallet |

Traditional brokerage account |

Private key management |

Investors are responsible for selecting an appropriate private key storage method. The investor must understand the technical and operational setup and associated risks. |

Cryptocurrency ETC issuer selects one or more specialized cryptocurrency custodians with institutional-grade private key custody operational and technical setups |

Liquidity |

Liquidity is fragmented across trading venues with varying liquidity levels |

Generally broader liquidity as multiple service providers (called “authorized participants”) have access to multiple trading venues |

Costs |

Vary, depend on specific setup, commonly include spreads, transactions costs and potentially custody costs |

Vary, but generally transparent fees, consisting of ongoing all-in fee (TER) and bid offer spreads that may be applied by your broker |

Xtrackers Galaxy Physical Cryptocurrency ETC securities

Xtrackers offers investors convenient exposure to bitcoin and Ether. Jointly with our strategic ally Galaxy, we offer cryptocurrency products (Exchange Traded Certificates) which are 1:1 physically backed. The cryptocurrencies are stored at one or more institutional-grade cryptocurrency custodians in “cold” offline custody solutions which unburdens investors from organizing safe private key management. The ETCs are issued by a Swiss issuer and are available for purchase at many brokers and banks across multiple European countries. The products are listed on the German stock exchange, Xetra. Investors can find more information about the products here.

Symbiotic partnership between Xtrackers and Galaxy

Xtrackers is the third largest European ETP issuer[3]. For more than 20 years, Xtrackers has been offering investors high-quality, convenient, and cost-effective access to all major asset classes. In particular, Xtrackers has a long and successful track record in building ETC platforms, providing investors access to precious metals, carbon certificates and now cryptocurrencies. Xtrackers has entered a strategic alliance with the publicly listed digital asset-native company Galaxy, which has deep cryptocurrency domain expertise. Xtrackers and Galaxy’s combined expertise enable to offer investors high-quality and cost attractive cryptocurrency exposure. Both companies focus on digital asset education to ensure that investors understand the innovative and exciting, but also complicated and risky cryptocurrency ecosystem.

Graphic: DWS International GmbH, 2024

Frequently asked questions

Where can I buy the Xtrackers Galaxy Physical Cryptocurrency ETC securities?

The products are distributed to investors via many traditional brokers and banks in multiple European countries, namely in Finland, France, Germany, Luxembourg, the Netherlands, Portugal, Spain, Sweden, and Switzerland. Institutional investors may in addition be able to directly purchase the products from one of several authorized participants.

What costs are associated with the Xtrackers Galaxy Physical Cryptocurrency ETC securities?

Investors will be charged two different costs. First, the ongoing product fee (TER) is competitively priced at 0.35%. Each ETC security is associated with a coin entitlement, which can be found here. The ongoing product fee is subtracted from the coin entitlement each day pro-rata. Second, investors will be charged a bid-ask spread when purchasing and selling the products. The bid-ask spread generally depends on the trading venue, the broker and prevalent market conditions.

How do ETCs differ from ETFs and ETNs?

ETCs, ETFs and ETNs all belong to the same product group of Exchange Traded Products (ETPs), that is financial instruments which are traded on a regulated stock exchange or via a market maker. Most ETPs are passively managed and track an underlying or an index. ETPs are very popular due to their high transparency and liquidity as well as their cost-efficiency.

The three product types differ in their legal structure. ETFs, that is Exchange Traded Funds, are fund structures where assets are segregated and thus investors should generally not bear issuer counterparty risks. ETCs, Exchange Traded Certificates or sometimes also referred to as Exchange Traded Commodities, and ETNs, Exchange Traded Notes, are debt obligations from the ETC / ETN issuer. ETCs are issued by an insolvency-remote Special Purpose Vehicle (SPV) that issues certificates backed by underlying assets (in our case cryptocurrencies). The insolvency remote SPV structure aims to reduce issuer insolvency risk. ETNs are also debt obligations like ETCs, however ETNs are issued from the balance sheet of an operating issuer, for example a bank or financial institution. Thus, investors need to consider the creditworthiness and financial stability of the ETN issuer’s operating business.

In continental Europe, cryptocurrency ETPs are mostly structured as ETCs or ETNs. In difference to the USA, the European UCITS regulation does not allow for single cryptocurrency ETFs. The Xtrackers Galaxy cryptocurrency products are structured as ETC secured debt obligations that are issued by an insolvency-remote Swiss domiciled SPV.

What are tax implications for German private investors?

Important note: The following assessment only refers to the basic tax classification of the Crypto ETC for private investors resident in Germany for tax purposes.

The Issuer believes that the Crypto ETC would not fall under the German flat tax regime (“Abgeltungsteuer”). Instead, the Crypto ETC should be taxed in accordance with the principles of the so called “private sales transactions” (“Private Veräußerungsgeschäfte”) due to sect. 23 para. 1 sent. 1 no. 2 German Income Tax Act (“EStG”) whereby a taxable event for a German private investor – applying its individual tax rate - should only occur if the period between acquisition and disposal / redemption would not exceed one year, considering the individual tax allowance amount according to sect. 23 para. 3 sent. 5 German Income Tax Act.

As the German flat tax regime should not be applicable (see above) the German custodian bank would not withhold any withholding tax and transfer it to the tax authorities. The taxpayer instead must file by itself and declare any capital gain within its individual tax return.

Please note that the above-mentioned remarks only could be seen as abstract description how the issuer individually would assess the legal status and its adaption by the German fiscal courts and the German tax administration without claiming correctness and completeness. The existing description only contains selected aspects of the German Income Tax Act and does not consider any changes which may occur as consequence of pending legislative measures, future administrative instructions or current legal proceedings. Therefore, any prospective investor urgently should consult its legal and/or tax advisors to take, considering its induvial circumstances, a suitable investment decision. The issuer would not assume any liability for the above-mentioned description and any investment decisions based on it.

Key advantages and risks of Xtrackers Galaxy Physical Cryptocurrency ETC securities

Key Advantages |

Key Risks |

|---|---|

|

Institutional-grade products: The product draws on the symbiotic expertise of Xtrackers and Galaxy, combining Xtrackers’ long-standing ETP track record[3] with Galaxy’s broad cryptocurrency domain expertise. |

Non-principal protected investments: Xtrackers Galaxy Physical Cryptocurrency ETC securities are non-principal protected investments, therefore an investor’s capital will be at risk up to a total loss. |

|

Convenience: A straightforward way to gain exposure to spot returns of the underlying cryptocurrency. The ETC security structure fits seamlessly into traditional brokerage accounts and portfolio management structures without the need to set up a cryptocurrency wallet. |

Distinct risks of cryptocurrencies: Prices of cryptocurrencies are extremely volatile when compared to most (if not all) traditional asset classes. Cryptocurrencies face distinct market, technical, operational, legal, regulatory, cryptocurrency custody, hacking, fraud and blockchain risks. |

|

Physical backing: The ETC securities are physically backed by the corresponding cryptocurrency, stored in institutional-grade cold storage cryptocurrency custody solutions at one or more cryptocurrency custodian(s). |

Market volatility affects investments: The value of the ETC securities depend on the underlying bitcoin/Ether price. It may go down as well as up and past performance is not a good indicator of future performance. |

|

Segregated wallets: Each ETC series has security over segregated cryptocurrency wallets held by the custodian(s) to ensure effective segregation of assets. |

Deduction of fees and no accrual of interest: Investments in cryptocurrency ETC securities will not accrue any interest and performance is subject to the deduction of the applicable fees. |

|

Minimal tracking error: Returns of the ETC securities are equal to the spot returns of the underlying cryptocurrency minus any applicable fees. |

Debt security: Investing in ETC securities will not make an investor the owner of the Underlying. |

|

Liquidity of Xtrackers ETC securities: Securities are traded intra-day on one or more major European stock exchanges. |

Secondary market pricing: Pricing of the ETC securities on the secondary market may be at a significant discount or premium compared to the Value per ETC Security (intrinsic value) published by the Issuer. |

|

Transparent value: The value of the ETC securities and the underlying cryptocurrencies are transparently reported on the Xtrackers website and news sources respectively. |

Exchange rate: The price of Cryptocurrencies is generally quoted in US dollars. If a security holder values cryptocurrencies in another currency, the value will be affected by changes in the exchange rate. |

Source: DWS International GmbH, 03/2024

For a full description of relevant risk factors, please refer to the prospectus.